ITA/ENG

How do different generations consume? Is Gen Z (the 18–28 age bracket) truly to blame for the collapse in spirits consumption in favor of No-Low Alcohol alternatives? And what does the future hold for the bar industry?

For some time now, these questions have been echoing through modern hospitality circles, where traditional bar talk has been replaced by deep analysis from industry operators and critics. These professionals are increasingly attentive to the exact direction in which the spirits market is moving.

All of us within the hospitality sector have noticed a significant crisis in consumption, attributing it to a wide range of factors. In Italy, the blame is often pinned on stricter blood alcohol limits for driving, a youth culture that doesn’t drink, struggling businesses, rising costs, geopolitical conflicts, and endless other excuses.

Just a few days ago, during an industry trade fair, while attending a panel discussion on the world of agave spirits, I was chatting with my dear friend and colleague, Jury Gelmini. Our conversation sparked after a question was posed to the panel of experts regarding how Generation Z approaches the bar scene today.

According to Jury’s intelligent and compelling theory, it is not true that Gen Z is consuming less; rather, they are consuming differently. His market analysis, drawn from direct firsthand experience and field observations, highlights that this generation has changed not so much what they drink, but how and where they drink it. Jury pointed out that in the past, socialization was deeply tied to physical meeting points in venues. The very foundation of gathering at a bar was dialogue—exchanging news or gossip—which generated the experience and, consequently, drove consumption.

Today, much of this social capital is preempted and captured by smartphones. Every piece of news, daily event, argument, or gossip leads users to exchange direct messages in real time. Consequently, very little is left to be said around a table or at a bar counter. Furthermore, the new generation tends to be more restrained in their public behavior due to contemporary behavioral and aesthetic standards. If in the past, without smartphones, what happened at the bar stayed at the bar (more or less), today any unusual or exuberant behavior can be shared instantly with a single click, risking immediate damage to a young person’s reputation or public image.

This is precisely where Jury’s analysis lands—and I completely agree with him: younger consumers have shifted a significant portion of their consumption within the walls of their own homes. The theory is straightforward: at home, among close friends, they feel free to consume whatever alcohol they desire, moving past generational constraints, appearances, or the pressure of public image management. They feel more at ease, surrounded by trusted friends in a safe environment.

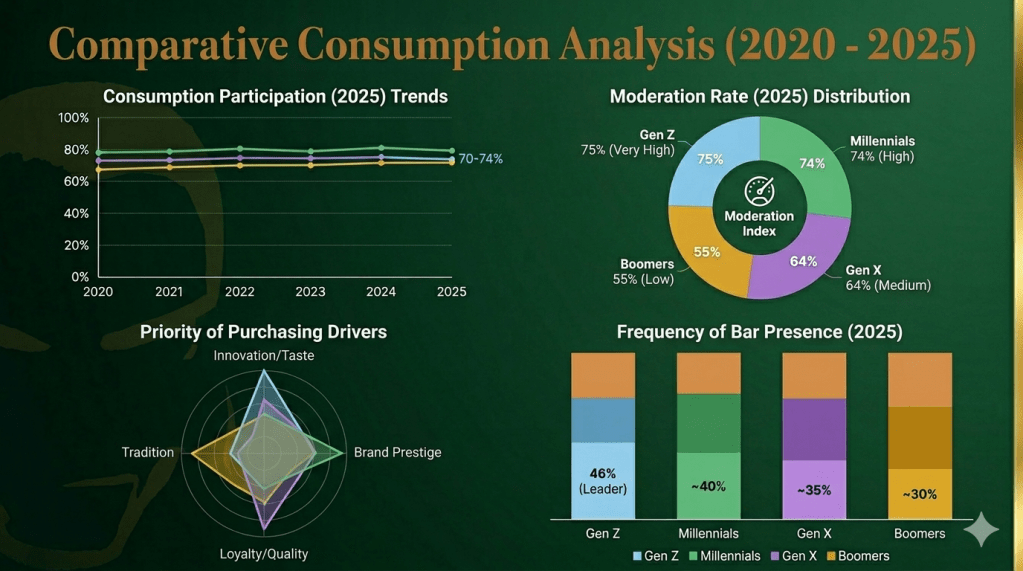

But what do global numbers and market reports actually say about this decline in consumption across different generations? We discover that currently, as of May 2026, Gen Z (those of legal drinking age) is no longer the primary “suspect” behind the market contraction. In fact, Millennials, Gen X, and Boomers have all radically altered their approach as well.

Here is what is emerging on a global scale:

1. Gen Z (Ages 18–28) — From Abstinence to “Social Moderation”

Gen Z has demonstrated the most radical shift. While they appeared entirely uninterested in alcohol between 2020 and 2022, recent data shows a highly targeted return to consumption.

- 2020–2022: A phase of low participation (around 46%). Heavily impacted by the “Sober Curious” movement and social isolation.

- 2023–2025: An increase in market participation, climbing to 70–74% by 2025.

- Behavior: They consume fewer categories per individual occasion, favoring image-driven products or innovative RTDs (Ready-To-Drink). They are the primary pioneers of “Zebra Striping” (alternating between alcoholic and non-alcoholic drinks throughout the same evening).

2. Millennials (Ages 29–44) — The Real Drivers of the No-Low Market

Millennials remain the most influential generation in terms of economic value, yet they are also the most focused on health and wellness.

- 2020–2021: A peak in home consumption of premium spirits and cocktail kits during lockdowns.

- 2022–2025: They became the leading buyers in the No-Low category, coming to represent 35% of that market.

- Behavior: 74% report that they regularly practice moderation. They are responsible for 30% of total industry spend, with their choices driven by brand prestige in 57% of cases.

3. Gen X (Ages 45–60) — The Stability of Great Classics

This demographic maintains the most consistent habits, showing only a slow, gradual transition toward higher-quality products.

- Evolution: They have maintained a steady spending share, accounting for 27% of the market.

- Behavior: They favor Whisky, Rum, and imported beers. Compared to younger cohorts, their consumption is more heavily tied to the home environment and loyalty to heritage brands.

4. Boomers (Ages 61+) — High Spending Power, Low Moderation

Unlike younger demographics, Boomers have not significantly reduced their consumption volumes over the past five years.

- Evolution: They hold the highest spending capacity, accounting for 36% of the total market.

- Behavior: Only 55% state that they moderate their consumption (the lowest percentage across all generations). They remain fiercely loyal to traditional categories such as Gin, Scotch, and Wine.

Conclusions

The most striking trend of the 2020–2025 period is the global convergence toward quality. While overall volumes are down slightly, spending per individual bottle has increased across every single age bracket (premiumization). Gen Z is no longer the “teetotal” generation of 2020; they have evolved into the generation of “drinking less, but better, and alternating.”

Diego Ferrari